Invity officially introduced their Turbo nákup (Turbo buy) service at last year’s Chaincamp, and I couldn’t pass up the chance to take a closer look at it.

Disclaimer: we have a long-term test collaboration with Invity. They have no say in the testing, and I’m doing it with my own money.

For readers who don’t know, I’d like to start by mentioning that Invity is part of the SatoshiLabs group, so it’s a “sister” of Trezor or Vexl. From its original role as an exchange and broker comparator that let you buy bitcoin at the best available price, Invity has shifted toward an app for saving into bitcoin using DCA. And the main draw – and possibly slightly controversial product – is Invity Turbo, which lets you buy bitcoin with someone else’s (borrowed) money. We’re still talking about DCA savings here, where you also have to put in your own money.

And even though it might seem a bit odd given the philosophy of the whole SatoshiLabs group, Invity is a fully regulated service under a MiCA license. That logically includes KYC. If you have a mental block about buying bitcoin with KYC, Invity isn’t the service for you, and you basically don’t need to read further. After all, the beauty of bitcoin is that you have a choice 🙂

Buying bitcoin with borrowed money

As mentioned, the main idea behind Invity Turbo is to give you a tool that’s commonly used by large corporations like Saylor’s (Micro)Strategy – namely, buying bitcoin with other people’s money. The idea is fairly simple – it bets that if I buy bitcoin today with borrowed money, then by the time I have to pay it back, bitcoin’s value will be higher than today, so to repay the debt I’ll only need to sell part of the bitcoin bought on credit, and the rest stays with me – that’s my profit.

A simple example: if I borrow 10,000 CZK today and buy bitcoin at a price of 1.3 million CZK per coin, and in five years sell half of those bitcoins at a price of 2.6 million CZK per coin, I’ll repay the debt and keep the other half of the bitcoins (for simplicity, let’s ignore interest, but even with it I’d still be in profit).

I’ll try Invity Turbo too

(with a lifetime 10% discount on fees)

How much Invity will lend you

According to Invity, they spent a long time testing and looking for a loan amount that would carry very low liquidation risk. You might know this from exchanges, where you can quite easily borrow high multiples of your capital, but the outcome tends to match that. The point is that the lender never loses money. The one who loses is always you. Even with a relatively safe x2 leverage, a 50% drop in bitcoin’s price wipes you out completely (and this happened in February, if you bought at the October ATH).

Another example: if you buy bitcoin for 10,000 CZK at a price of 1.3 million per coin, where 5,000 is yours and 5,000 is borrowed, then if bitcoin’s price drops to 650,000 CZK, your bitcoins are suddenly worth only five thousand and must be sold to repay the 5,000 loan – the lender loses nothing, you lose everything.

That’s why Invity Turbo’s “leverage” is only x1.6. This means that for every 100 CZK of your own money, Invity lends you another 60 CZK. Based on historical data, with this level of leverage liquidation reportedly would never have occurred over the past ten years. This is partly because we’re still talking about DCA purchases, so your purchase price keeps averaging out, and even drops of tens of percent don’t lead to liquidation.

So if you’re saving, say, 1,000 CZK every two weeks, Invity will automatically make an additional 600 CZK available alongside it. Or rather, you won’t get exactly 600 CZK, but somewhat less, because a fee for borrowing it is deducted (to make things more complicated, the fee is charged on the crowns borrowed in the past – for the ones borrowed today, you pay for the first time only with your next payment). The longer you save with Invity Turbo and the more money you have borrowed, the more gets deducted in fees from each payment. After a year of saving, about 105 CZK gets deducted, so you effectively only get 495 CZK lent to you.

I admit this is a bit complicated to wrap your head around, but you can see all the fees clearly in the app. For the skeptics and doubters, I’d recommend playing around with it in Excel.

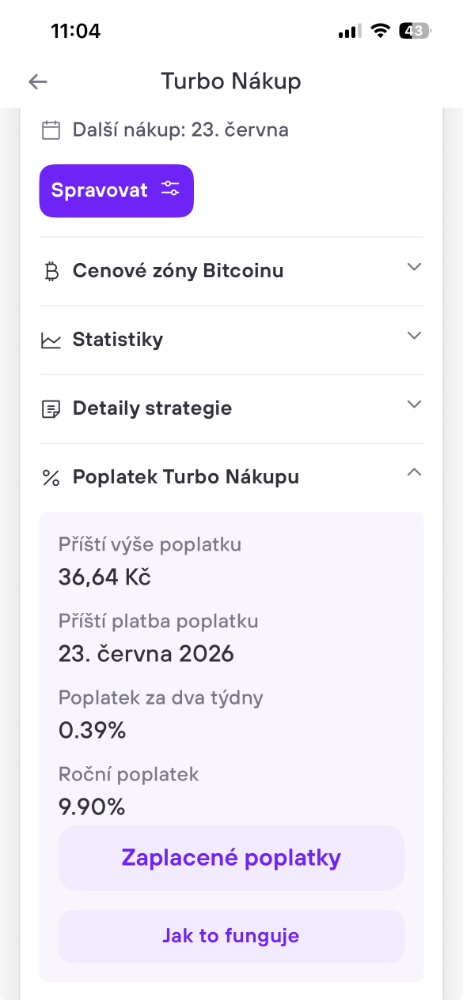

How much it costs to borrow

Currently it works out to 9.9% per year. That’s not exactly nothing, but considering the service started at 14%, it’s become bearable. If that still seems too much to you, you don’t have to use the offer. Also, from conversations with people at Invity, the goal is to bring interest rates down over time, so even 9.9% might not be the final state.

In the app you can see the current interest rate, but in practice it mainly works with fees on each purchase. These consist of two parts:

- Service fee for the purchase, which is 0.49% for a SEPA payment and 1.49% for a card payment (cards are penalized because about 1% goes to the card issuer)

- A percentage of your payment: ~0.83% for monthly frequency, ~0.39% for biweekly frequency, or ~0.19% for weekly payments. This is charged starting from the second purchase.

The Turbo fees are shown clearly in the app:

Could it be cheaper? Sure. You could take out a bank loan at 5% and then handle DCA manually, for example through Štosuj. But don’t forget that you have to repay a bank loan continuously every month, whereas Invity Turbo only at the end of the saving period. Plus you borrow the entire sum upfront, but with DCA it sits there and you allocate it to bitcoin gradually – yet you pay interest on the whole amount.

Similarly, you could pledge your bitcoin via Firefish and use the borrowed fiat to buy more bitcoin. But if that’s what you want to do, you’re probably not Invity’s target audience. That audience is more likely people who don’t want to deal with anything complicated and often won’t even be hardcore bitcoiners, but rather beginners who simply want to save into bitcoin and use a bit of light leverage along the way.

How to set up Turbo savings

First you need to install the Invity app on your phone. If you’re reading this article on a computer, you can also use this QR code to get directed to the mobile install (using my link or QR code gives you a lifetime 10% discount on fees):

After installing the app, on first launch you need to go through identification (KYC), because as mentioned, Invity is a regulated entity and must comply with anti-money-laundering and counter-terrorism-financing laws, among others.

Verification for Invity is handled by a third party – the company Sumsub – and consists of the standard photographing an ID document and taking a selfie. After that you have to answer a few standard questions, such as whether you’re a politician, where your source of income comes from, how much you plan to invest through Invity, and so on. The whole thing takes no more than 5 minutes, and if you’ve ever verified an account on an exchange or broker, it’s exactly the same.

Once verified, you can set up your savings strategies. In addition to Turbo, you also have access to regular DCA and its plus variant, which optimizes purchases based on the development of the 120-week moving average (something similar to what Štosuj does in its advanced DCA strategies). But for the purposes of this review, we’re interested only in the Invity Turbo variant, so select that one.

In the settings you can then choose how often you want to buy bitcoin and how you want to pay for it. For the interval, you have a choice of weekly, biweekly, and monthly. It’s definitely good to buy as often as possible, but decide based on how much you want to save in total per month. Each transaction must be at least 750 CZK, so if you want to save, say, the equivalent of 1,000 CZK per month, you have no choice but to pick the monthly interval. If you have two thousand per month, choose the biweekly interval and always send a thousand.

As for how to pay, you have a choice of either card payment or bank transfer. I recommend choosing transfer, because card payment costs you more – it carries that extra 1% fee mentioned above.

But watch out for one annoyance I find hard to understand – for transfer payments, the minimum isn’t 750 CZK, but 1,250. The reason given is that card payments are charged to the provider as a percentage, while SEPA carries a fixed fee. And since for testing purposes I wanted a higher frequency than once a month, while also not wanting to pay unnecessary card fees, I chose 1,250 CZK every two weeks. You can change the amount and frequency later in the settings.

After saving your settings, the app shows you where to send the money. If you chose card payment, the funds come from your card and you don’t need to worry about this. For transfers, you pay to a Czech account as usual. It’s just an account at the Citfin savings cooperative, so it doesn’t support instant payments (but a transfer sent in the morning from mBank showed up in Invity by lunchtime). However, thanks to the MiCA license, a “normal” bank should be added soon. The simplest setup is to create a standing order for the date the app shows you.

One slightly confusing thing is that the date shown by Invity doesn’t actually matter. The bitcoin purchase happens whenever the money arrives at Invity. It doesn’t matter if you send it earlier or later – it just might confuse the app a bit. For example, I was supposed to send money on the 10th, it arrived on the 9th, and the app was still showing as of the 15th that it was waiting for the payment from the 10th. So it’s best to just send the money the way the app expects 🙂 I’ve been told by Invity that this “bug” should be fixed soon.

And that’s it. Once you set up Turbo buying, you don’t need to do anything else – just send the money to Invity on the right date.

How to keep an eye on liquidation

This is explained and illustrated perfectly in the app. You can see how risky your current savings position is, when you’ll get which warning, and when liquidation would occur.

How to end Turbo

I’ll really only test this part in a few years, since this is a long-term test. But for now, here’s the theory at least. You can end the savings plan at any time, which means you have to repay the debt and all fees. The debt is repaid by Invity selling part of your bitcoins needed to cover the debt expressed in crowns. You can see how much you owe directly in the app. Note that ending the savings plan after just a few weeks doesn’t make much sense, because you’ll likely come out behind purely on fees. The magic of DCA is that it works better the longer you run it. So thinking about ending the plan makes more sense after several years. But you really can do it at any time.

In the future, there should also be an option to settle the debt with a separate fiat payment – the advantage being that this wouldn’t trigger a taxable event for the user, which currently happens when bitcoin is sold.

And watch out – as long as Turbo is active, you can’t send the purchased bitcoins to your own wallet, because they need to remain available in case the debt has to be settled. This is different from standard DCA, where you can transfer your purchased bitcoins to your wallet immediately, and even automatically. With Turbo, Invity doesn’t hold your bitcoins directly itself, but hires a professional “custody” company, BitGo, which manages over $100 billion in assets this way.

What my long-term test looks like

As mentioned, I’m testing Invity Turbo long-term, buying bitcoin for 1,250 CZK every 14 days since December 29, 2025. You can follow how my savings are doing in a public Google spreadsheet – here I’m just including a screenshot of it. I also post observations about the test regularly on my Twitter (X), and I’d be happy if you followed me there.

As of June 9, 2026, I’ve bought 0.01569248 BTC, for which I put in my own 16,250 CZK, with another 9,750 CZK borrowed from Invity. The purchased bitcoins are now worth 20,300 CZK, so I’m currently down 22%. But it’s important to remember that a loss is normal during a bear market – and the numbers will look that much nicer during a bull market 🙂 For more detail, see the Google spreadsheet.

Conclusion

I won’t evaluate the savings result here. I’m convinced that in the long run it always ends up positive. But only time will show the reality.

Invity Turbo is, in my view, a great idea, and technically it works flawlessly. It’s probably not a service for hardcore bitcoiners or financial specialists, who could design something similar themselves. But for people who know a little about bitcoin and want to save into it using more than just plain DCA, while not wanting to manage leverage themselves, I think it’s a good service and I recommend trying it. And if they manage to bring down the cost of borrowed money, it’ll be even better.

Pros

- operator credibility – not a no-name startup, but a company from the SatoshiLabs holding (makers of Trezor)

- a relatively safe way to buy bitcoin on credit

- transparent communication – you know what you’re paying and what you get for it

- Czech-language app

- rapid development – the app improves with every update

- the service is supervised by the Czech National Bank (ČNB) – holds a MiCA license

Cons

- higher cost of borrowing capital

- the fee structure can be harder for a layperson to understand

I’ll try Invity Turbo too

(with a lifetime 10% discount on fees)