Obsah článku

- 1 Don’t borrow at the ATH

- 2 Never borrow against all the bitcoin you have

- 3 Take several smaller loans with different maturities

- 4 Don’t borrow for too long

- 5 Lock more collateral than required

- 6 Early-repay your best-collateralised loan first

- 7 If two loans are threatened with liquidation, consider topping up only one

- 8 The infinite loan doesn’t work well in a bear market

- 9 Deal with everything early and in advance

Firefish I’ve been using for a long time — I was even one of the beta testers back when access to the platform was invite-only and not everyone could join. I have quite a bit of experience by now, and the recent 50% drop in bitcoin from the current ATH gave me the idea to write up some tips and tricks for sleeping soundly with a Firefish loan. Especially in a bear market.

If you’re not familiar with Firefish, make sure to read my extensive and regularly updated review. You’ll find out how it all works, why it’s exceptionally safe and how to get a discount on the fee for your first loan: Firefish – a loan against bitcoin collateral [REVIEW]

Disclaimer: what’s described below doesn’t apply universally. Everyone is in a different life situation, borrows for different reasons, different amounts, has a different bitcoin reserve and a different risk tolerance. Take these tips as loose inspiration, but run the numbers for your own situation.

TIP: Haven’t tried Firefish yet? On your first loan, you can get a 30% fee discount from me. The standard fee is 1.5% of the borrowed amount, so for you just 1%. Try a loan with a discount.

So let’s get to those promised tips and tricks.

Don’t borrow at the ATH

This is advice I commonly hear, but I’d rather refine it to don’t borrow at the ATH – and if you do, be prepared that you might run into trouble. It always depends on your specific situation and why and how much you’re borrowing. And of course the problem is that you don’t know you’re at the ATH – or rather you know it, but you never know whether it will turn tomorrow and a bear market begins, or whether the ATH will be 30% higher next month.

If you’re “lucky” enough to time the turn and bitcoin only goes down from the moment of your loan, you need to account for the fact that a 50% drop puts your loan at risk of liquidation. In reality it takes a slightly smaller drop – a loan gets liquidated at 95% LTV (borrowed amount + interest / collateral value). So it’s good to follow the next recommendation as well.

Moje nová kniha nejen pro začátečníky

Stahujte ukázku zdarma, nebo si rovnou kupte plnou verzi. S kódem deset-dolu ji máte o 10 % levněji.

Never borrow against all the bitcoin you have

This is probably the most important rule. You never know what will happen over the life of the loan and whether a big price drop will come and you’ll need to top up your collateral to avoid liquidation. If you can’t top it up, the loan can end in liquidation – your bitcoin gets sold, the lender gets their money back and you’re left with nothing.

A variation on this rule is to keep some cash on the side for early repayment in an emergency, though that doesn’t make much sense – if you have the cash, why borrow more. Or keep some cash on the side to buy bitcoin and send it as additional collateral. That can make sense, because you took out the loan at some price and if liquidation is threatening, bitcoin is clearly tens of percent cheaper, so buying it and topping up the collateral is a good deal.

Take several smaller loans with different maturities

If you need to borrow a larger sum – say 100,000 CZK – I think it’s better to take, for example, two loans of 30,000 and one of 40,000, with maturities spread across different timeframes, say 3, 6 and 12 months. Why?

A Firefish loan, including interest, is repaid at the end. You pay nothing monthly, which is nice, but only until the loan matures – at that point you need to send the lender the full amount. And if you don’t have great self-discipline and don’t regularly set money aside for repayment, it can be a lot easier to repay a relatively small sum than one big hit.

On top of that, a repaid loan can immediately be rolled into a new loan, so if the repayment fits within your regular cash flow – for example the total doesn’t exceed your monthly income – you can simply repay the loan from your paycheck and take out a new one right away. No cash flow headaches. Just be aware that if bitcoin has dropped in the meantime, you’ll need more BTC to roll the loan over – so see the tip above: keep bitcoin in reserve.

Yes, you might lose a little on interest because loans of different lengths have different rates, but the peace of mind is worth it in my opinion.

Don’t borrow for too long

This is a very personal tip, but personally I never really understood the calls for multi-year loans (the current maximum at Firefish is 2 years). In my opinion a year is a reasonable maximum, because so much can happen in bitcoin over a longer period that it might not be pleasant. In a bull market you might have unnecessarily much bitcoin locked up for two years, and in a bear market you’ll have too little and need to top up. The bull market scenario is worse because there’s nothing you can do about it (apart from early repayment). A shorter loan means freedom for me – I can react faster to the current situation.

Lock more collateral than required

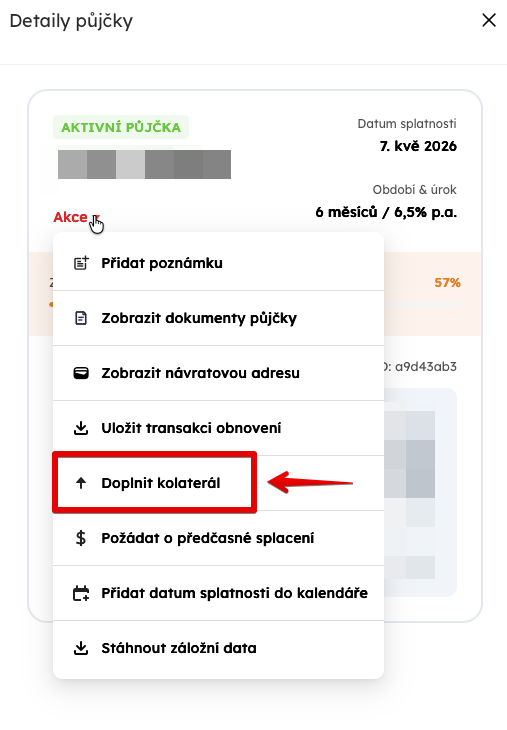

I don’t think this is widely communicated publicly, but at the moment of taking out a loan you can send collateral in any amount (larger than what Firefish asks for). For example, if you’re closing a loan and Firefish tells you to lock 0.1 BTC, you can send 0.15 BTC without any special arrangement or permission. You’ll have significantly more collateral than needed and your liquidation threshold will be much lower than if you only sent the required 0.1 BTC.

This is obviously useful for people who have relatively a lot of bitcoin, know they won’t need it anytime soon and want to sleep soundly. That said, you can sleep just as soundly locking only the required amount and topping up the collateral only when the price drops to a level that starts making you nervous. You can top it up at any time:

Apparently people commonly do this and over-collateralise right from the start. The Firefish guys confirmed it when they were on our Bitcoin a blondýna podcast (czech language only).

Early-repay your best-collateralised loan first

If your loans are heading into trouble, your dashboard is flashing that loan health is approaching zero and you can’t or don’t want to top up collateral, you have another option: early repayment. Your instinct might be to repay the most at-risk loan, but that’s not necessarily the best move. It can be better to early-repay the healthiest loan – or at least a very healthy one – because that releases the most collateral in crown value, which can then be used to top up the most at-risk loan, or even multiple at-risk ones.

Be aware though that early repayment takes time – you first need to submit a request and the lender has to approve it. They have no reason to refuse – they get all their interest and their money back sooner – but it can happen that they’re not online at that moment and don’t approve it right away. And even after approval, a bank transfer still needs to go through and the lender has to confirm receipt. Only once that confirmation happens and Firefish marks the loan as closed can you breathe easy.

If two loans are threatened with liquidation, consider topping up only one

When everything is falling apart, liquidation warnings are flashing on multiple loans, you have no fiat for early repayment and only a limited amount of bitcoin to top up collateral – consider whether it might be better to put all your bitcoin into one loan’s collateral and let the other one go, accepting that liquidation may happen. You never know how far the price drop will continue, and it’s quite possible that if you add a little collateral to two loans, a continued price drop liquidates both. If you try to save just one, there’s a chance you push its liquidation value down far enough that it survives even a further significant bitcoin price drop.

This is advice for when you’re already in serious trouble and just trying to minimise losses. If you stick to the rules above, you shouldn’t find yourself in this situation.

The infinite loan doesn’t work well in a bear market

The infinite loan is something that works beautifully when the bitcoin price is rising. You borrow 100,000 CZK and lock bitcoin worth 200,000. The price rises and at repayment time the collateral is worth, say, 220,000. You repay 105,000 including interest, get back bitcoin worth 220,000 and borrow 100,000 again, for which locking 200,000 worth is enough. So 20,000 worth of BTC is left unlocked. After subtracting interest you’re 15,000 ahead.

The theory says that bitcoin goes up long-term and as long as it rises by more than the loan interest, you never have to repay it and you’ll always be ahead. But it’s obvious that once the bitcoin price is falling, the infinite loan stops working – or rather it only works if you keep adding more bitcoin to the collateral. Because if the price drops, you borrowed 100,000 against collateral worth 200,000, and when the collateral value falls to 180,000, you’re 20,000 short on collateral for a new 100,000 loan after repaying the old one.

Deal with everything early and in advance

Don’t wait – act early. As we saw just recently in February, bitcoin can drop tens of percent within a few hours even in 2026 and gives you no chance to address problems as they develop. If you let your loan health fall to 10% and only then start working on early repayment, it might not work out at all – because that’s a process that takes days, not hours. And topping up collateral isn’t a matter of minutes either. As if on cue, you’ll hit a period when blocks are slow to mine or fees spike briefly and your top-up transaction doesn’t go through for several hours.

When it comes to topping up collateral, it’s worth remembering that you’re not losing it – it all comes back to you. So it’s definitely better to top up unnecessarily early than to wait until the last minute and miss the window.

PS: Liquidations on Firefish actually did happen at the start of February, so this isn’t theoretical.

TIP: Haven’t tried Firefish yet? You can now get your first loan completely fee-free. The standard fee is 1.5% of the borrowed amount. Try a loan with no fee.

Čtěte dále:

- Firefish Review 2026: Bitcoin-Backed Loans Without Selling Your BTC [REVIEW]

- DCA Bitcoin Savings with Invity Turbo [Review + Lifetime Fee Discount]

- Don’t miss the dream deal – set your alerts to TradingView.com (INSTRUCTIONS)

Líbil se ti článek? Ukaž jak moc 😉

1. Zvol částku · 2. Klikni na „Poslat přes Lightning"

Naskenuj QR mobilní Lightning peněženkou

nebo pošli přímo na: Nevím, která bije

powered by DonateBySatoshi